The Corridor Capital

Geography as Credit: How Infrastructure Corridors Are Repricing Sovereign Access to Capital Markets

The Premise

There is an axiom at the center of sovereign debt analysis that we have encountered, in different forms, across most of the work we have published here. It goes something like this: a country’s borrowing cost reflects its institutions, its fiscal trajectory, and its political risk. Geography, in this framework, is passive, a background variable that shapes trade flows but does not, by itself, determine the terms on which a government raises capital.

That axiom is being quietly revised, and we think the revision deserves more systematic attention than it has received.

Over the past three years, a pattern has emerged across three distinct geographies, sub-Saharan Africa, Central Asia, and the broader Middle East, that we find structurally significant. Sovereign states that would ordinarily occupy the speculative fringe of international capital markets are accessing financing at improved terms, attracting multilateral guarantees, and issuing instruments into London and international markets, not because their macroeconomic fundamentals have been transformed, but because they sit astride corridors that powerful states have decided they cannot afford to see fail.

The corridor has become a credit instrument. Our argument here is that this dynamic is not incidental, not temporary, and not yet fully priced.

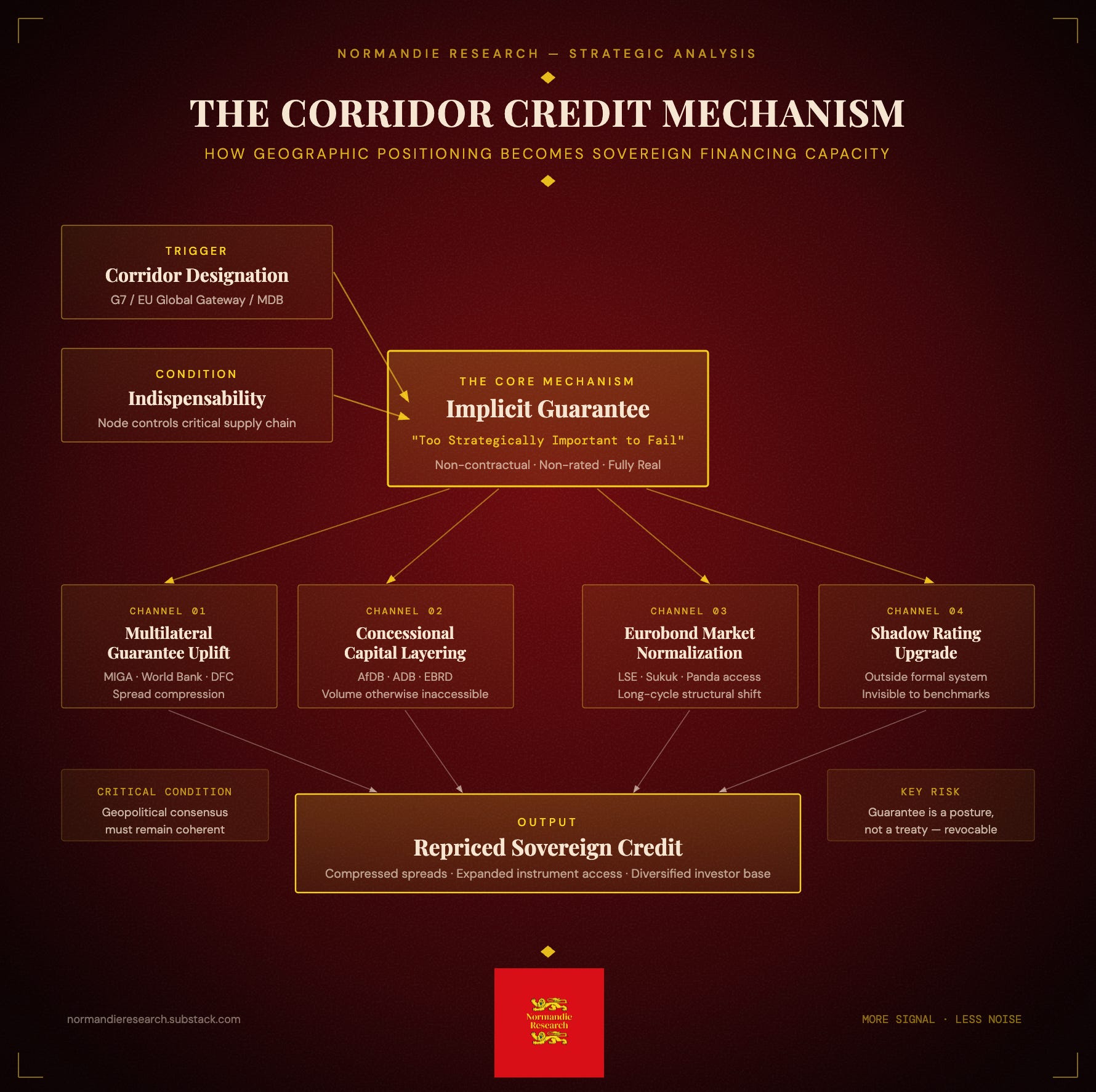

The Mechanism: How a Corridor Becomes Collateral

Before examining the cases, we want to be precise about the financial architecture. “Geography as credit” can sound like a metaphor; we mean it as a description of specific, traceable mechanisms.

The corridor-as-credit-instrument operates through several distinct but mutually reinforcing channels.

Multilateral guarantee uplift

When a corridor is designated a strategic priority, by the G7, the EU’s Global Gateway, or a major development finance institution, it triggers a cascade of guarantee instruments. MIGA coverage, World Bank guarantees, DFC backstops: these reduce the effective credit risk on sovereign borrowing, compressing spreads independently of sovereign fundamentals. Angola’s December 2024 London issuance was not priced on Angola’s underlying fiscal position alone. It was priced, in part, on the institutional backstop that the Lobito designation had unlocked.

Concessional layering

Strategic corridor status redirects concessional capital that would otherwise be inaccessible or heavily conditioned. Zambia, still working through its own sovereign debt restructuring, benefits from the AfDB’s commitment and the World Bank’s subsequent package, volumes that a non-corridor Zambia would be unlikely to attract on similar terms.

Eurobond market access normalization

The more durable effect is longer-cycle: sustained corridor investment and the associated multilateral presence gradually normalizes a sovereign’s footprint in international debt markets. Kazakhstan’s sovereign bond issuances, Azerbaijan’s recent credit upgrades, and Angola’s active evaluation of sukuk and panda bonds alongside conventional Eurobonds all reflect this dynamic. Azerbaijan and Kazakhstan have both received significant credit rating upgrades from all three major agencies in recent cycles, a shift that is not entirely separable from their deepening entrenchment as indispensable corridor nodes.

The geopolitical implicit guarantee

Perhaps most consequentially: when a transit state becomes structurally important to the supply chains or strategic objectives of a major power, that state acquires an implicit backstop that no rating agency model fully captures. If Angola defaults, Lobito stalls. If Kazakhstan destabilizes, the Middle Corridor fragments. The corridor creates a non-contractual guarantee, a “too strategically important to fail” premium, that compresses sovereign risk in ways that remain largely invisible to conventional analysis.

This last mechanism connects directly to arguments we made in Rated Sovereign, Treated Pariah, where we observed that the real verdict on sovereign creditworthiness is increasingly issued not by formal rating agencies but by the market actors and institutional structures that sit behind them.

The corridor is one of the cleaner examples of this phenomenon: the multilateral and geopolitical architecture around Lobito or the Middle Corridor is effectively a shadow rating upgrade, operating outside the formal system but no less real in its financial consequences.

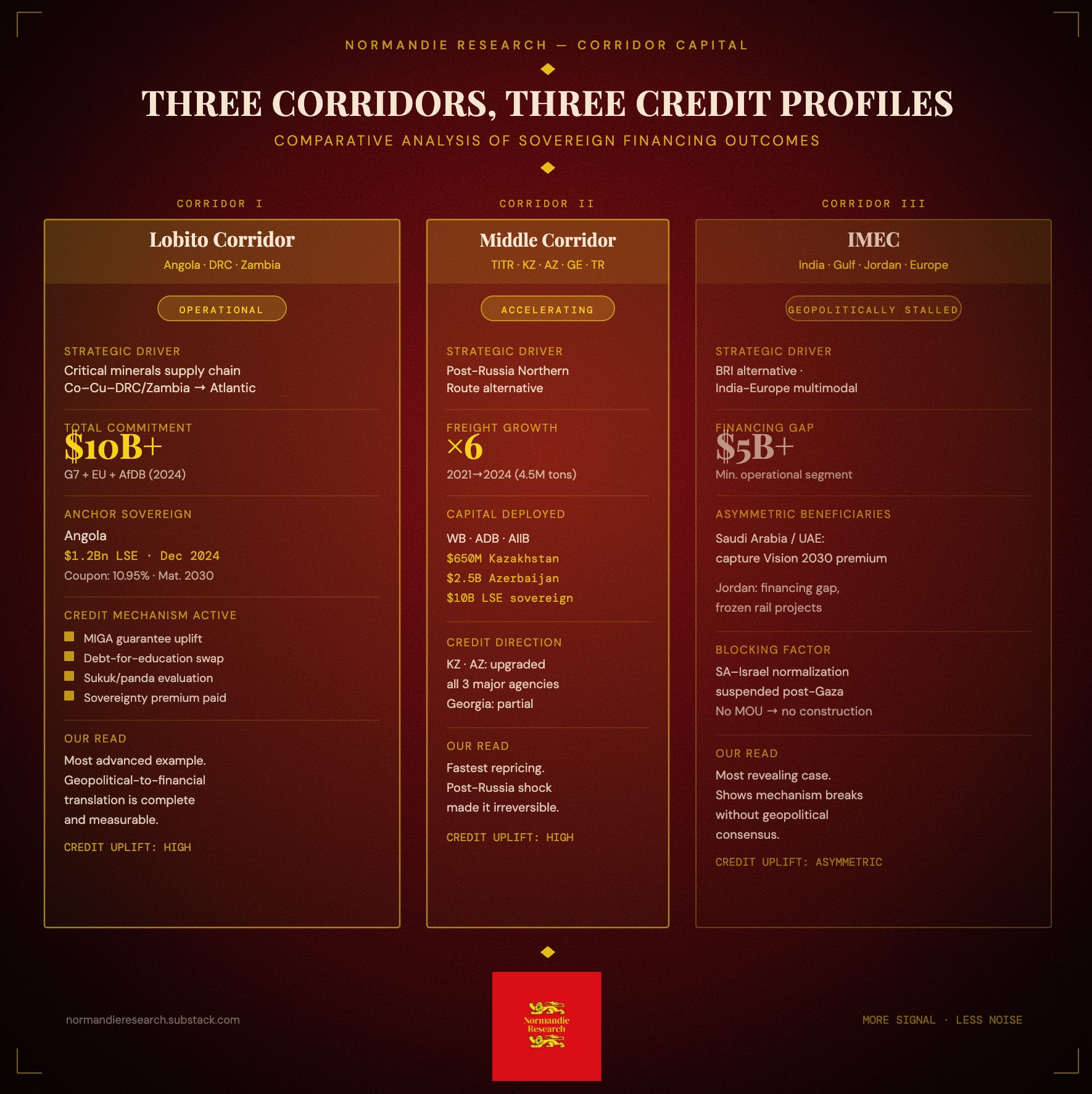

Case I — The Lobito Corridor: Geography as Geopolitical Arbitrage

The Lobito Trans-Africa Corridor connects Angola’s Atlantic port to the copper belt of Zambia and the cobalt basin of the DRC, the two countries that together account for a dominant share of the global supply of minerals essential to the energy transition. The corridor is, structurally, a critical mineral supply chain instrument dressed as a development infrastructure project. We think it is worth being explicit about that framing, because it is precisely what explains the scale and speed of Western capital deployment.

The Benguela Railway was rehabilitated through 2014 under a $2 billion oil-backed infrastructure deal with China, before its strategic significance was reasserted as Western powers sought an Atlantic alternative to eastbound routes. In 2022, Angola awarded a 30-year concession to a Western consortium, Trafigura, Mota-Engil, and Vecturis, committing more than $550 million in rolling stock and operational upgrades.

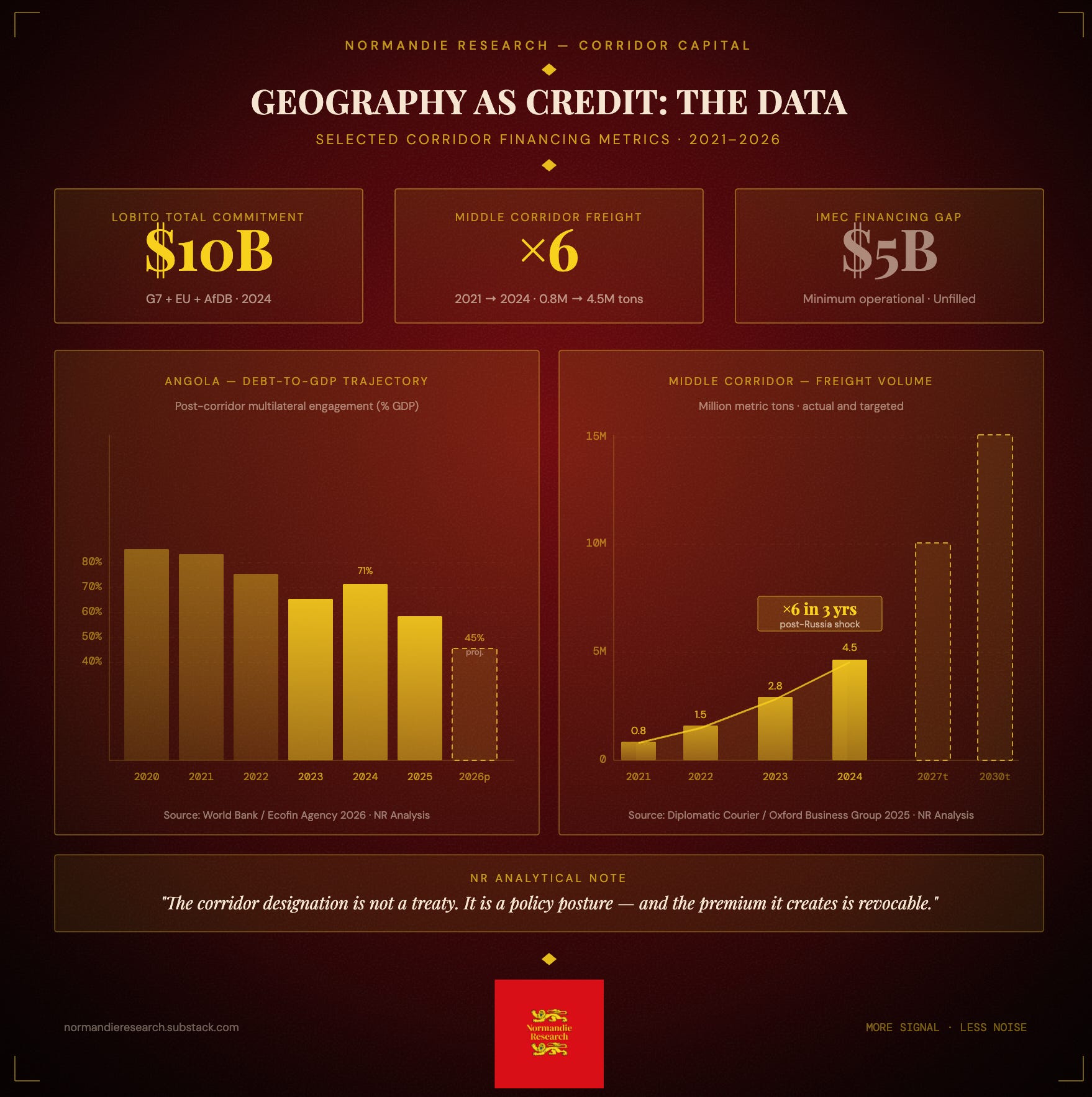

What followed is instructive. The United States, European Union, and African Development Bank collectively pledged more than $10 billion in infrastructure and support programs. US commitments alone exceeded $4 billion by late 2024. The World Bank committed $500 million to the new Zambia-Lobito greenfield rail project in November 2023, followed by a further $650 million loan, bringing total multilateral investment above $1 billion in twelve months.

The financial consequence for Angola has been direct and measurable. In December 2024, Angola issued $1.2 billion in Treasury notes on the London Stock Exchange, due 2030 at a coupon of 10.95%. Expensive, certainly, but accessible. A country with Angola’s oil-revenue dependency, its historical Chinese debt overhang, and its ongoing fiscal consolidation would not, in a pre-corridor environment, have accessed London markets on this basis. Angola has been systematically dismantling oil-collateralised Chinese loans and replacing them with market-priced capital, paying what analysts have called a “sovereignty premium” in exchange for operational flexibility and geopolitical non-alignment.

We think the debt-for-education swap is the most eloquent illustration of the mechanism. The World Bank approved MIGA guarantees supporting an arrangement that allows Angola to repurchase up to $400 million of expensive commercial debt and replace it with cheaper guaranteed financing, with savings redirected toward school construction. This is the corridor at its most consequential: not merely enabling infrastructure financing, but restructuring the entire cost of capital stack of a sovereign whose access to such instruments, absent strategic corridor status, would be far more constrained.

Angola is also evaluating alternative bond formats, sukuk, panda, and samurai instruments, to diversify its investor base toward Asia and the Middle East. The corridor has created the credibility surface on which these instruments become viable, and this is precisely the normalization dynamic we want to track over the next two to three years. It is not Angola’s macroeconomic transformation that makes panda bonds possible. It is Angola’s geopolitical positioning.

Case II — The Middle Corridor: The Post-Russia Revaluation

The Trans-Caspian International Transport Route, connecting China’s eastern coast to Europe via Kazakhstan, the Caspian, Azerbaijan, Georgia, and Turkey, is the case we find most analytically interesting, because the credit repricing is happening fastest, in the most measurable way, and in sovereigns whose structural position in Western financial markets was previously limited.

The Middle Corridor would have remained a niche freight alternative were it not for February 2022. Russia’s invasion of Ukraine did not merely disrupt one trade corridor. It revealed the structural fragility of the Northern Route and simultaneously elevated every state that could offer an alternative, a dynamic that maps directly onto arguments we developed in The Weaponized Dollar about how geopolitical ruptures force infrastructure and capital to find new paths simultaneously.

The Middle Corridor provides the shortest rail route connecting Europe and China, approximately 3,000 kilometers shorter than alternative northern routes. Freight volumes surged from 800,000 tons in 2021 to 4.5 million tons in 2024, a near-sixfold increase in three years. Kazakhstan is targeting 10 million tons by 2027 and 15 million tons by 2030.

The capital translation has been swift. In November 2024, the World Bank approved $650 million for the Transport Resilience and Connectivity Enhancement Project in Kazakhstan, the first joint World Bank–Asian Infrastructure Investment Bank project in the country.

In November 2025, the Asian Development Bank committed up to $2.5 billion to support Azerbaijan’s development priorities through 2029, and approximately $5.4 billion for Kazakhstan’s development goals over 2026–2029.

The sovereign bond dimension is where we think the most significant signal lies. At a high-level conference on Caspian transport connectivity in London in 2025, UK Trade Envoy Lord John Alderdice outlined UK support for raising $10 billion through sovereign bonds on the London Stock Exchange, with direct assistance to Kyrgyzstan and Kazakhstan. The London Stock Exchange is not, historically, a venue associated with Central Asian sovereign paper. This matters. It suggests that the corridor designation is not merely attracting development finance, it is opening primary capital market access that these sovereigns did not previously have. That is a qualitatively different kind of repricing.

Kazakhstan, Uzbekistan and Azerbaijan are each advancing infrastructure investment programmes aligned with the corridor’s expanding role, with multilateral financing from the World Bank, EBRD and Asian Development Bank providing the capital and governance frameworks to address persistent bottlenecks.

There is a structural subtlety worth isolating here. The Middle Corridor transits multiple jurisdictions: Kazakhstan, Azerbaijan, Georgia, Turkey. Each benefits from the aggregate traffic, but the credit effects are asymmetric. Kazakhstan, as the primary overland node, receives the most direct multilateral attention. Georgia, smaller, more fragile, geopolitically exposed, benefits from corridor traffic without acquiring the same multilateral backstop. This asymmetry is precisely what we observed in Rated Sovereign, Treated Pariah: the formal system treats corridor-adjacent states as a category; the real financial system differentiates them by indispensability.

Case III — IMEC: The Corridor That Hasn’t Been Built, and What That Reveals

IMEC, the India-Middle East-Europe Economic Corridor, is the most instructive case precisely because it is the least operational.

Launched at the 2023 G20 summit in New Delhi, IMEC encompasses three pillars: a transportation backbone integrating rail and maritime networks, an energy pillar with cross-continental electricity and energy infrastructure, and a digital pillar providing fiber-optic cables and cross-border digital connectivity. It is, on paper, an extraordinarily ambitious corridor, connecting the world’s most populous nation to the world’s largest single market via the world’s most hydrocarbon-rich region.

In practice, nearly two years after its G20 launch, IMEC had no clear funding structure, no unified authority, and no binding financial commitments, a collection of memoranda of understanding with no confirmed dollar figures attached. The corridor’s transportation segment faces a financing gap of approximately $5 billion to become minimally operational, with most unmet costs concentrated in Jordan, Israel, and logistics hubs in Saudi Arabia.

The Gaza conflict suspended normalization talks between Israel and Saudi Arabia, and Jordan faces significant economic difficulties, reflected in the freezing of a joint electricity project with Israel and delays in securing railway upgrade financing.

We believe IMEC’s partial failure is analytically as important as Lobito’s partial success, because it reveals where the mechanism breaks down. The geopolitical guarantee only functions if the geopolitics are coherent. IMEC’s core weakness is that it depends on a Saudi-Israel normalization that the regional conflict has indefinitely suspended. Without that normalization, the corridor’s most valuable segment, the overland link across the Levant, cannot be built. And without that segment, the corridor cannot generate the traffic flows that would justify the capital commitment. The implicit guarantee requires an implicit consensus that does not, for now, exist.

Yet IMEC’s very designation has already produced financial effects for its Gulf anchor states. For Saudi Arabia, IMEC is viewed as an integral part of Vision 2030’s economic diversification mandate. In May 2025, PIF and I Squared Capital signed an MOU to establish a dedicated infrastructure investment strategy focused on the Middle East, explicitly designed to accelerate investment in key infrastructure sectors and build connectivity across regional and global markets.

This is the IMEC dynamic in its most exposed form: the financial benefits of corridor designation accrue asymmetrically, favoring states that already have sufficient institutional credibility to attract capital on the promise of future connectivity, Saudi Arabia, the UAE, while states that need the corridor most remain hostage to geopolitical sequencing they cannot control. Jordan is, in this framework, the anti-Angola: a state that is nominally on the corridor but cannot monetize that position because the corridor’s realization requires political conditions it cannot produce.

The contrast with Priced for Exclusion is worth noting.

In that piece, we argued that Indonesia faced a systematic discount on its sovereign financing capacity despite solid fundamentals, because the frictions of custody, settlement, and index inclusion created an access gap invisible in the rating. IMEC’s weakest-link states face a structurally similar problem from the opposite direction: they are theoretically included in a corridor with transformative financing implications, but the practical frictions of geopolitics prevent them from accessing those implications.

The Limits of the Framework

We want to be careful not to overstate the case: the corridor-as-credit-instrument is real, but it is not without failure modes, and we think intellectual honesty requires naming them.

Geopolitical contingency is non-diversifiable

Angola’s Lobito position depends on sustained Western strategic interest in critical minerals. If that interest shifts, through technological substitution, a minerals supply glut, or a change in US foreign policy priorities, the implicit guarantee evaporates. The corridor designation is not a treaty. It is a policy posture, and policy postures change. We have seen, in The Rationing Interval?, how quickly physical market dynamics can diverge from the structural narratives that underpin investment positions.

The same risk applies here.

Fiscal fundamentals do not disappear

Corridor status can compress spreads and unlock multilateral access. It cannot resolve structural fiscal imbalances. Angola’s debt-to-GDP ratio is projected to decline to approximately 45% by 2026, from roughly 71% in 2024, but that improvement reflects oil prices and domestic fiscal consolidation as much as corridor financing. A sovereign that borrows on corridor credibility without repairing underlying fundamentals accumulates a fragile liability structure. The corridor is a financial lever, not a fiscal solution.

The indispensability premium is not divisible

A corridor transiting five sovereigns does not distribute its credit effect evenly. Kyrgyzstan benefits from the Middle Corridor narrative without receiving Kazakhstan’s multilateral capital flows. The credit benefit accrues to nodes, not neighbors, and the market has not yet fully internalized this distinction.

Construction risk is real

The Zambia-Lobito greenfield rail line, 800 kilometers built from scratch, targeted early 2026 for groundbreaking. The credit benefit of corridor designation is front-loaded; the corridor’s ability to sustain that benefit depends on eventual physical operationalization. We are watching.

What We Think This Means

We began this piece by saying the old axiom, that geography is passive in sovereign credit analysis, is being revised. We think the revision is structural, not cyclical, and that it will outlast the current geopolitical moment.

The corridor is not a new idea. What is new is the speed and explicitness with which Western institutions have decided to mobilize infrastructure as a financial instrument in the competition with Chinese-led connectivity models.

The Lobito concession, the Middle Corridor bond ambitions, the IMEC G20 launch: all of these are, at bottom, exercises in using the promise of geographic integration to compress the financing cost of strategically important sovereigns.

For investors, the implications are directional. Corridor-node sovereigns deserve a systematic re-examination of their spread compensation. If Angola, Kazakhstan, and Azerbaijan are structurally better-backstopped than their standalone credit profiles suggest, their current spreads may embed implied risk that has been partially but not fully revised. The asymmetric intra-corridor distribution of credit benefits creates relative value opportunities: states that are logistically indispensable but institutionally underrated are a more interesting expression of this theme than the headline anchor states.

Most consequentially, and this is the argument we find ourselves returning to most, the corridor framework requires investors to track geopolitical commitment signals with the same attention they give to fiscal data. A deterioration in G7 strategic interest in critical mineral supply chains, or a shift in US posture toward any of these corridors, would reprice corridor-node sovereign credit faster than any fiscal variable. The geopolitical guarantee is real. It is also revocable.

The corridor has become a financial instrument. Reading it requires a different set of tools than the ones sovereign credit analysis has historically provided.

Normandie Research publishes independent strategic analysis. Nothing in this piece constitutes investment advice, a recommendation, or a solicitation to buy or sell any security. Figures are drawn from company filings and public reporting as of June 2026 and are subject to change. Readers are responsible for their own decisions.

This is a great and highly insightful article. Congratulations to the authors for such an excellent piece of analysis.

One point worth emphasizing is that what many market participants still perceive as arbitrariness is often better understood as discretion exercised by political actors. Investors and financial analysts are being forced to adapt to a new paradigm in which geopolitics and great-power competition have become central drivers of economic outcomes. As economic statecraft moves to the forefront of the international financial system, foreign influence, industrial policy, sanctions, export controls, and national security considerations increasingly shape capital allocation and market dynamics.

However, many observers continue to analyze these developments through a purely economic lens, underestimating how profoundly political considerations now influence financial markets. Hopefully, articles like this one will help them put two and two together.