Priced For Exclusion

Indonesia, MSCI, and the gap between what the market prices and what the facts support.

Before We Start.

Normandie Research is an independent strategic analysis publication for institutional investors, executives, and serious private investors who have run out of patience for financial noise.

We publish long-form analyses at the intersection of geopolitics, economic statecraft, capital flows, commodities, and financial markets. When there is nothing worth saying, we say nothing. When there is, we build the argument from the ground up.

Every piece challenges a prevailing narrative, every trade thesis is constructed, not asserted. The signal, from the noise, is the service.

Some pieces from us:

MSCI-Bye-Bye Indonesia

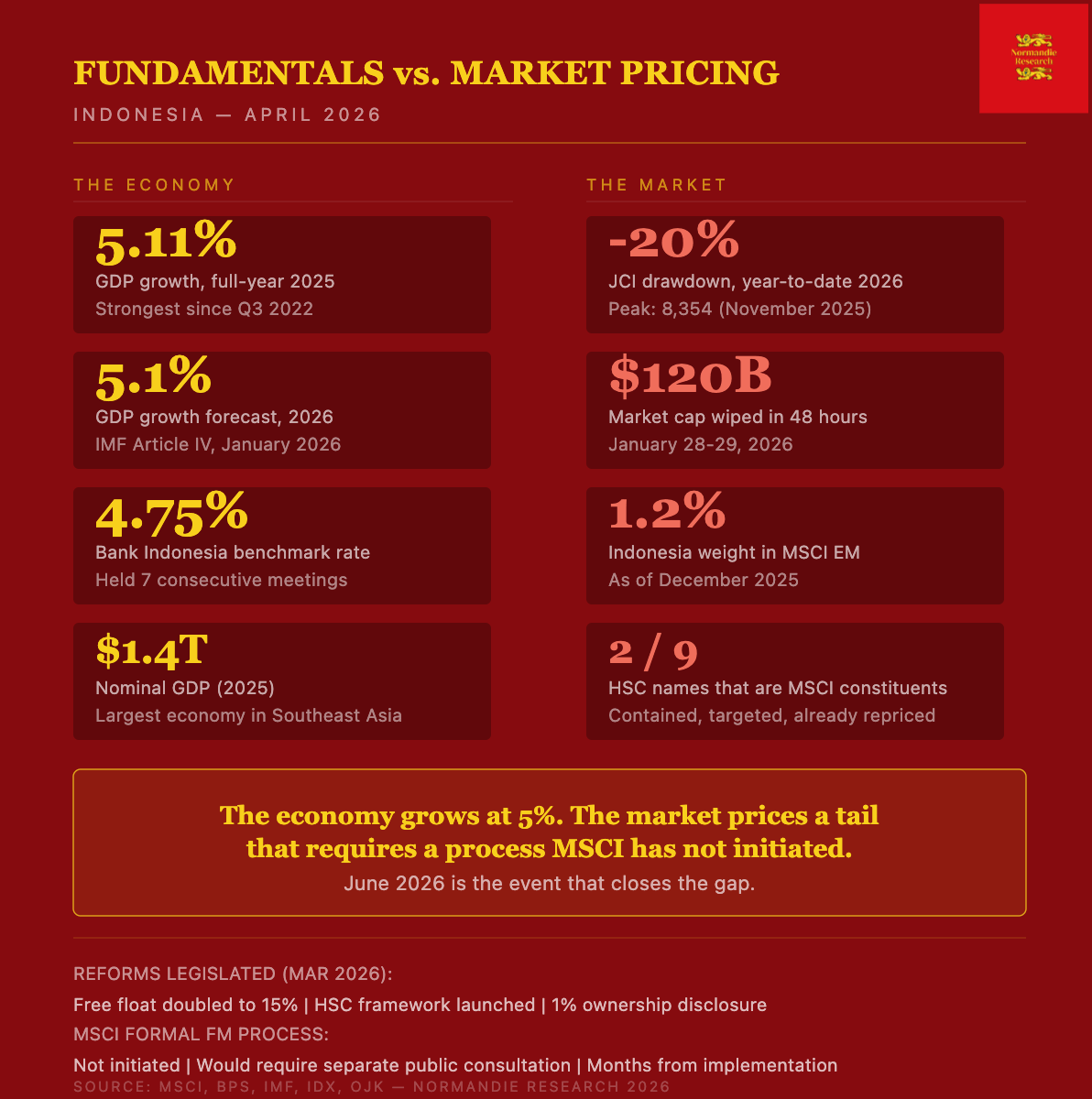

On January 28, 2026, MSCI did something it rarely does: it publicly threatened a G20 economy with frontier market reclassification. In the two sessions that followed, Indonesia’s stock market shed approximately $80 billion in market value. The January warning ultimately erased approximately $120 billion from the Jakarta market across the full selldown period. Two senior regulators lost their jobs. Concern about an MSCI downgrade has seen the nation’s key index slide about 20% this year.

The cause was a transparency letter from a private index provider, and the passive-flow mathematics that accompany it.

MSCI concluded that ownership data for Indonesian equities remained insufficiently transparent. The firm flagged unclear ownership structures, high ownership concentration, and risks of coordinated trading that could distort price formation.

The underlying issue: a local trading practice known as goreng-goreng saham, which involves shares changing hands among affiliated parties to generate artificial price momentum before being offloaded to retail investors, combined with conglomerate ownership chains opaque enough to make accurate free-float estimation unreliable.

MSCI’s threat was explicit. Failure to improve transparency and establish a credible monitoring system for ownership concentration by May 2026 could lead to a reduction in Indonesia’s weight in the MSCI Emerging Markets Index, or even a downgrade to frontier market status.

The binary that every fund desk priced immediately: EM to Frontier Market, triggering an estimated $10 to $11 billion in net outflow from Indonesian markets, mostly contributed by companies currently in the MSCI Standard Cap index, with funds mandated to hold only EM-classified assets forced to exit.

That binary has not materialized. More importantly, it almost certainly will not. The market has not fully processed this.

What MSCI Actually Said, and What It Did Not

It is worth reading MSCI’s January announcement carefully, because the market largely did not.

MSCI did not initiate a formal reclassification review. It froze positive index adjustments, meaning no new inclusions, no upward size migrations, no increases to Foreign Inclusion Factors. It also stated explicitly, buried beneath the headline threat, that any formal reclassification from Emerging Market to Frontier Market would require a separate public consultation with market feedback before implementation. This is a multi-step, multi-month process.

The precedents MSCI itself has cited for historical downgrades, Peru, Argentina, Pakistan, share nothing with Indonesia’s situation: those prior downgrades involved an inability to meet quantitative investability requirements such as having fewer than three qualifying companies, government capital controls, or floor-price rules, rather than a disclosure methodology dispute.

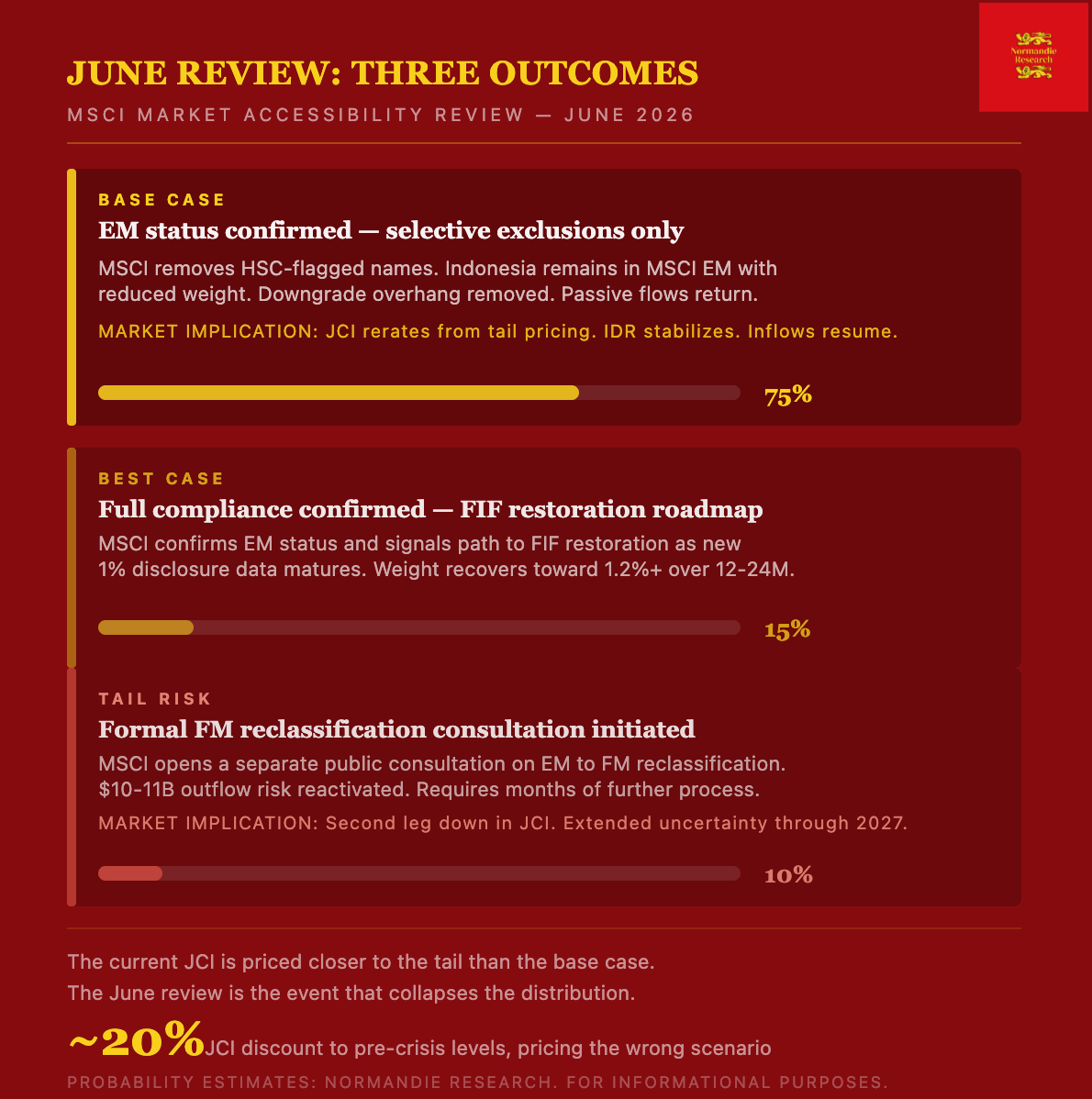

What MSCI described as the worst-case scenario was conditional on zero progress by May 2026. Even in that scenario, a formal downgrade deliberation would have been a separate event, likely pushing any actual reclassification into 2027 at the earliest. The market priced the tail on day one. That is the setup.

The Reform Response

Indonesia’s regulatory response was faster and more substantive than most observers expected from a market characterized by entrenched family conglomerate dominance. President Prabowo was reportedly furious at the market’s reaction. That anger, whatever its private texture, translated into legislative urgency.

By March 31, 2026, amendments were made to Indonesia’s stock exchange rules that included the doubling of free-float requirements to 15 percent and the expansion of disclosure thresholds. The Indonesia Stock Exchange simultaneously introduced the High Shareholding Concentration framework, publicly naming the nine companies with ownership concentrations above 95 percent, and committing to regular ongoing disclosure.

The ownership reporting threshold for individual shareholders was lowered to 1 percent, a material improvement in granularity over the prior 5 percent threshold.

These are not cosmetic adjustments. The doubling of minimum free float is the structural change MSCI’s consultation specifically identified as necessary. The HSC framework directly addresses the coordinated trading concern. The 1 percent disclosure threshold addresses the beneficial ownership opacity concern.

MSCI’s response to these reforms was to remove Indonesian stocks with high ownership concentration from its indices while postponing its review of the country’s market status by one month to assess the effectiveness of recently announced regulatory reforms.

Critically, the only securities it moved against in the May cycle were the two most egregious cases: Barito Renewables Energy, owned by billionaire Prajogo Pangestu, and Dian Swastatika Sentosa, part of the Sinar Mas conglomerate controlled by the Widjaja family. These are bounded, named, already-repriced risks.

The expert consensus that has emerged is clear. “We don’t think Indonesia will be downgraded to frontier market and it will stay in the emerging-market category,” said Henry Wibowo, a former JPMorgan strategist who co-founded Alphagate Capital in Jakarta.

Allspring Global Investments’ portfolio manager sees the decision to extend the review as reducing the immediate risk of a downgrade from emerging market status. “It suggests Indonesia is broadly moving in the right direction, with MSCI seeking additional time to assess the scope and consistency of updated disclosures,” he said.

Allianz Global Investors’ head of equity for Indonesia noted that “recent actions by Indonesian authorities, particularly enhanced ownership disclosure and the introduction of a high shareholding concentration framework, address MSCI’s core concerns around transparency and investability, which reduces the probability of a downgrade.”

What the Market Is Pricing

Concern about an MSCI downgrade has seen the nation’s key index slide about 20% this year, even as regulators have raised free-float requirements and asked for more shareholding disclosures. Indonesia’s MSCI EM weight sits at approximately 1.2 percent.

The $10 to $11 billion outflow figure has been the anchor since January. It is the worst-case number, the full passive exclusion from EM mandates. It requires a formal FM reclassification. It requires a public consultation MSCI has not initiated. It requires several months of additional process. And it requires that the reforms Indonesia has already legislated prove entirely without effect.

The expected removal of Barito Renewables and Dian Swastatika Sentosa “reflects a prudent and targeted application of its high shareholding concentration framework, rather than a broader negative assessment of the Indonesian market,” according to Allspring’s portfolio manager. The individual-security exclusions have been priced at the stock level. They have not been distinguished from the index-level tail risk in the JCI selldown. That distinction is where the trade lives.

The gap between a managed, bounded weight reduction in MSCI EM and a full FM reclassification is enormous in equity market terms.

The JCI appears to still be pricing something between those two outcomes, closer to the tail. The June Market Accessibility Review is the event that forces the distribution to collapse.

The Fundamentals Beneath the Noise

Something worth stating directly: the MSCI compliance crisis has no fundamental economic cause. Indonesia’s underlying economy has not deteriorated.

Indonesia’s economy grew by 5.11 % in 2025, higher than the achievement in 2024, which grew by 5.03 percent. Growth accelerated in Q4 2025 to 5.39 percent year-on-year, the strongest yearly growth since Q3 2022, boosted by solid private consumption on continued government support measures and lower borrowing costs. The IMF, completing its Article IV consultation in January 2026, described Indonesia as “a global bright spot, with strong economic growth amid a challenging external environment.”

Bank Indonesia held its key rate at 4.75 percent for a seventh consecutive month, focusing on supporting the rupiah amid persistent capital outflows. The current account deficit remains contained. Government debt-to-GDP is low by any regional comparison.

The rupiah has weakened to approximately Rp 17,140 per dollar, under combined pressure from global risk-off and the Indonesia-specific capital outflow from the MSCI situation. This creates an additional layer of return potential: IDR recovery is a free option attached to equity rerating for any foreign investor who enters at current levels.

Indonesia’s $1.4 trillion G20 economy is structurally too large, too liquid, and too economically significant to be treated as a frontier market in any durable sense. The country is the largest economy in Southeast Asia. Its capital markets have the depth and breadth of an emerging market with legitimate long-term institutional interest. The precedents MSCI itself has historically applied to FM downgrades simply do not map to Indonesia’s situation.

The compliance issue is a disclosure methodology dispute.

It is not a question of investability in any fundamental sense.

MSCI is asking Indonesia to show it who owns what.

Indonesia has begun doing that. The process of verification is what takes time.

The Note on Timing

A correction to the framing that has circulated since January, including in this publication’s earlier tracking of the story: the definitive decision date is June 2026, not May.

MSCI said Monday it is examining the scope, consistency and effectiveness of new data sources and regulatory measures announced by Indonesia’s financial authorities. The company will provide additional updates in a June review. The May semi-annual index review did produce action, specifically the removal of the two HSC-identified MSCI constituents, but the full market accessibility assessment has been extended to June. MSCI said it will continue to engage with market participants and relevant authorities in Indonesia and expects to have more to say during its market accessibility review in June.

This one-month extension should be read as signal, not noise. Gary Tan at Allspring characterized it directly:

“It suggests Indonesia is broadly moving in the right direction, with MSCI seeking additional time to assess the scope and consistency of updated disclosures.” An extension is not the language of an organization preparing a downgrade.

The Setup

The trade is not complicated. It is the gap between what a market prices and what the facts support.

A market that sells off 20% on an index methodology compliance issue, while the underlying economy grows at above 5%, while the issuing authority has legislated the structural reforms specifically requested, and while the analytical consensus from every major regional desk with skin in the game rejects the downgrade scenario, is a market that has allowed mechanics to override fundamentals. The mechanics drove the selldown. The mechanics will drive the rerating.

Overall, experts agree that Indonesia is going in the right direction, even if near-term index flows may create volatility at the individual stock level. “Active investors remain engaged, and Indonesia continues to be viewed as an important EM exposure, particularly once the transitional phase around index methodology adjustments is absorbed,” noted AllianzGI’s Indonesia equity head.

The key challenge remains a market dominated by family-owned conglomerates that operate dozens of listed and private entities from mining and tobacco to petrochemicals, with control typically maintained through relatives and related parties. This is not a challenge that disappears on a June announcement. It is a structural feature of Indonesian capital markets that MSCI will continue to monitor over years. But it is a challenge that Indonesia has, for the first time, agreed to address systematically, and the trajectory matters more than the starting point.

The worst-case scenario, a formal FM downgrade, remains a process MSCI has not initiated and would require months of additional deliberation to implement. The base case, a partial weight reduction managed through targeted individual-security exclusions, is a dramatically better outcome that the current price does not reflect.

June is not far.

A Note on the Structural Constraint That Remains

This analysis is not a call for complacency on the underlying structural problem, because the underlying structural problem is real.

The top 20 largest tycoon-linked companies on the Jakarta Composite Index make up nearly 43% of its weighting, including PT Bank Central Asia and PT Bayan Resources. They also make up about half of the MSCI Indonesia Index. The disclosure reforms that have been legislated are necessary conditions for MSCI’s continued confidence. They are not sufficient conditions for a clean capital market. The goreng-goreng saham practice does not disappear because the stock exchange now publishes a list of high-concentration names. Monitoring is not the same as enforcement.

The proposed reform package is a necessary but insufficient step if it remains purely technical. Concrete policy actions should include linking access to accelerated public listings or state-backed financing to verifiable investments in the real economy, while higher disclosure thresholds and exchange demutualisation improve transparency but must move beyond reactive compliance.

Citigroup’s strategist in Jakarta has noted that “the May 2026 MSCI semi-annual index review may still bring about selective exclusions or weight reductions for stocks flagged with high concentration,” and that the expected removal of the two MSCI-constituent HSC names “will effectively lower the free float” on a bounded basis.

This is the honest version of the base case: some weight reduction, managed at the individual-security level, while the broader market re-rates from tail pricing to base-case pricing. Not a clean bill. Not a restoration of full FIF increases. But a decisive step back from the edge that the current JCI price does not reflect.

TL;DR

The weight reduction is priced.

The frontier market risk is not justified.

That is the gap.

This analysis is published for informational purposes and does not constitute investment advice. All trade data and market figures are sourced from public disclosures and should be independently verified before any investment decision.

Normandie Research — April 2026

$120 billion wiped on a transparency letter from a private index provider. Not a central bank. Not a regulator. Not a sovereign credit downgrade. An index company that technically just curates a list.

The goreng-goreng detail is the kind of thing that never makes it into the headline but explains the entire trade. Coordinated price manipulation through affiliated party transactions dressed up as market activity. MSCI basically said "we can't tell what's real volume and what's theatre" and the market heard "frontier downgrade" because that's the scarier word.

The gap between what MSCI actually said and what the market priced is where this piece earns its keep. A freeze on positive adjustments is not a reclassification. But $80 billion in two sessions says the market didn't read past the first paragraph.

That's the trade if you believe the May consultation produces something workable.